Your Payment Processor Can Freeze Your Money. Ours Can't.

In November 2022, FTX collapsed. $8 billion in customer funds — gone. Not hacked. Not stolen by outsiders. Just... gone. Because customers trusted a company to hold their money, and that company turned out to be untrustworthy.

You might think that's a crypto exchange problem, not a payment processing problem. But the architecture is the same.

When you use Stripe, PayPal, or any traditional payment processor, your customers pay them. They hold the funds. They decide when to release them to you. And if they decide to freeze your account — for any reason, at any time — your money is locked.

This isn't hypothetical. It happens constantly.

The Account Freeze Problem

Search "Stripe account frozen" or "PayPal funds held" on any forum. You'll find thousands of stories from legitimate businesses who woke up one morning to find their revenue locked with no explanation and no timeline for resolution.

Why it happens:

- Automated fraud detection flags your account (false positive)

- A spike in volume triggers a risk review

- A single chargeback pushes you past an internal threshold

- You're in a "high-risk" category (which includes most digital goods and international businesses)

- Regulatory changes in a jurisdiction you sell to

What happens next:

- Your funds are held for 90-180 days (sometimes longer)

- You can't process new payments

- Customer support gives you templated responses

- You have no legal recourse beyond small claims court

- Your business bleeds cash while you wait

This is the counterparty risk of custodial payment processing. You're not just paying fees — you're trusting a company with your entire revenue stream. And that trust can be broken unilaterally, without warning, without explanation.

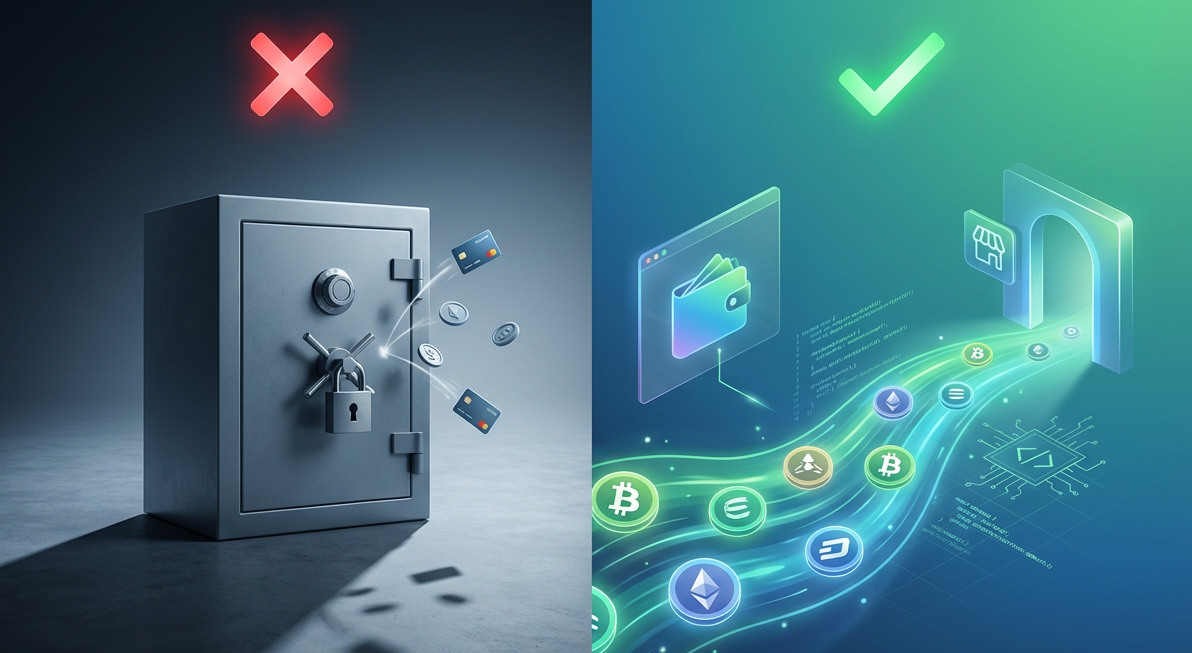

What "Non-Custodial" Actually Means

Non-custodial means the payment processor never touches your money.

With QBitFlow, when a customer pays you, the funds move directly from their wallet to yours. Not to QBitFlow's wallet. Not to an escrow account. Not to a holding pool. To you.

QBitFlow's role is infrastructure — smart contracts that facilitate the transaction, APIs that trigger billing events, dashboards that show you analytics. But at no point does QBitFlow have access to, custody of, or control over your funds.

This isn't a policy. It's architecture. The smart contracts are open-source. You can read the code and verify that there is no mechanism for QBitFlow to redirect, hold, or freeze funds. It's not that we choose not to — it's that we can't.

The Practical Differences

Custodial (Stripe, PayPal, BitPay)

Customer → pays → Processor → holds funds → pays you (eventually)

- Processor receives the money first

- Processor decides when to release it (2-7 days, sometimes longer)

- Processor can freeze funds at any time

- Processor can reverse transactions (chargebacks)

- If processor goes bankrupt, your funds are at risk

- You need to trust the processor's solvency, security, and good faith

Non-Custodial (QBitFlow)

Customer → pays → You (directly, via smart contract)

- You receive the money immediately

- No one can freeze it after receipt

- Transactions are final (no chargebacks)

- QBitFlow's financial health is irrelevant to your funds

- Trust is in the code, not the company

"But I Trust Stripe"

Fair. Stripe is a well-run company with a strong track record. Most businesses using Stripe will never have their accounts frozen.

But "most" isn't "all." And the businesses that do get frozen are often the ones that can least afford it — growing startups with spiky revenue, international businesses with diverse customer bases, digital goods sellers with above-average dispute rates.

The question isn't whether you trust Stripe today. It's whether you want your business architecture to require that trust.

Non-custodial payment processing removes the trust requirement entirely. Your funds are yours the moment the transaction confirms. No company — not QBitFlow, not anyone — can change that after the fact.

The FTX Lesson Applied to Payments

FTX wasn't the first custodial failure, and it won't be the last. The crypto industry learned a painful lesson: "not your keys, not your coins" isn't just a slogan. It's a risk management principle.

The same principle applies to payment processing.

When a custodial processor holds your revenue, you're exposed to:

- Operational risk — their systems go down, your payments stop

- Solvency risk — they go bankrupt, your funds are in the creditor queue

- Policy risk — they change their terms, your business model becomes "high-risk" overnight

- Regulatory risk — a regulator in their jurisdiction freezes operations

Non-custodial eliminates all four. Your payment infrastructure doesn't depend on any single company's continued existence, good behavior, or regulatory standing.

How QBitFlow Makes It Work

The technical challenge of non-custodial payments is handling recurring billing. One-time payments are straightforward — customer sends, merchant receives. But subscriptions require someone to initiate the charge each billing cycle.

Traditional processors solve this by storing card details and charging them on schedule. That's inherently custodial — they need access to the payment instrument.

QBitFlow solves it with authorized spending caps. The customer signs a smart contract that says: "This merchant can pull up to X tokens from my wallet every Y days." The authorization lives on-chain. QBitFlow triggers the pull at each billing cycle, but the smart contract enforces the rules — amount limits, frequency limits, and the customer's right to revoke at any time.

The merchant gets predictable recurring revenue. The customer keeps their funds in their own wallet until the moment of billing. And QBitFlow never has custody of anything.

The smart contracts are open-source. Every authorization, every payment, every cancellation is verifiable on-chain. This is transparency you can audit, not transparency you have to take someone's word for.

Who This Matters For

If you're a Web3 business

Your customers already have wallets. They already understand non-custodial. Using a custodial payment processor for a Web3 product is architecturally inconsistent — and your users will notice.

If you sell internationally

Custodial processors add cross-border fees, currency conversion charges, and higher fraud scrutiny for international transactions. Non-custodial doesn't care about borders. A payment from Tokyo settles the same as a payment from Texas — instantly, at the same 1.5% fee.

If you've been burned before

If you've ever had funds frozen, an account suspended, or a payout delayed at the worst possible time — you already know why this matters. Non-custodial means never worrying about it again.

If you're building something that needs to last

Businesses that depend on a single custodial provider have a single point of failure. Non-custodial payment infrastructure is more resilient by design — it doesn't depend on any one company's continued operation.

The Trade-offs (Honest Assessment)

Non-custodial isn't magic. There are real trade-offs:

Your customers need crypto wallets. If you're selling to mainstream consumers who only have credit cards, QBitFlow isn't a replacement for Stripe — it's a complement. Offer both. Let crypto-native customers pay with wallets, and everyone else pay with cards.

You receive crypto, not fiat. Payments settle in USDC, USDT, EURC, ETH, SOL, or other supported tokens. If you need dollars in a bank account, you'll need an off-ramp (exchange or service that converts crypto to fiat). For businesses already operating in crypto, this is a non-issue.

Smart contract gas fees. On Ethereum mainnet, gas fees for subscription operations can be meaningful for small transactions. On Solana, they're negligible (fractions of a cent). Choose the chain that fits your transaction profile.

Fewer integrations (for now). Stripe has plugins for everything. QBitFlow has API + SDKs (TypeScript, Python, Go) and a no-code web app. E-commerce plugins (WooCommerce, Shopify) are coming. If you need a Shopify plugin today, you'll need to wait or build a custom integration.

The Bigger Picture

The payment processing industry is built on a model where intermediaries hold your money and charge you for the privilege. That model made sense when there was no alternative — someone had to sit between the customer's bank and yours.

Blockchain removes that requirement. Smart contracts can enforce payment terms without holding funds. Transactions can settle instantly without a clearinghouse. And open-source code can provide transparency that no corporate policy ever could.

Non-custodial payment processing isn't just a feature. It's a fundamentally different architecture — one where you don't have to trust anyone with your revenue.

Your money should be yours the moment your customer pays. That's not a radical idea. It's how payments should have always worked.

QBitFlow is non-custodial crypto payment infrastructure for Ethereum and Solana. Open-source smart contracts, 1.5% flat fee, instant settlement. See how it works →

Related Articles

Why Non-Custodial Matters: The Hidden Risks of Letting Payment Processors Hold Your Crypto

Custodial payment processors can freeze your funds, go bankrupt, or get hacked — and there's nothing you can do about it. Here's why non-custodial crypto payments are the only model that actually protects your business.

Read more